|

Impact of Second Trump Presidency on Latin America

Impact of tariffs and immigration policy on currencies and economic growth.

BY JOLYN DEBUYSSCHER

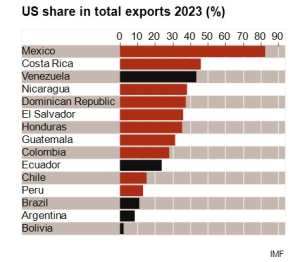

Flat import tariff would mainly hurt countries without free trade agreement

During his election campaign, president-elect Trump promised harsher trade policies and protectionist measures. One of his key trade policy proposals is to implement a flat import tariff of 10 to 20% on all US imports. Even though it is not certain yet if the measure will be (fully) implemented, as the threat could serve as a bargaining chip for other concessions, it would negatively impact countries that heavily rely on exports to the USA. As shown in the graph below, mainly Central American countries would be impacted in Latin America, with Mexico exporting about 85% of its goods to the USA. However, countries that have a free trade agreement with the USA (indicated by the red bars on the graph) are expected to be largely shielded from these US tariffs.

That being said, despite the United States-Mexico-Canada Agreement (USMCA), Mexico is likely to be slapped with (temporary) US tariffs on certain exports. As in his first presidential term, president-elect Trump is highly concerned about countries that have a large trade surplus with the USA. Last year, Mexico had the largest surplus with the USA, after China. Moreover, China might want to use Mexico as a backdoor to export its goods to the USA and avoid tariffs on Chinese goods, or build factories in Mexico for the same reason. Consequently, Mexico will be high on Trump’s agenda, alongside China, which is likely to lead to high tensions between the two neighbouring countries. Although a break of the free trade agreement is unlikely, president-elect Trump could try to fully renegotiate the USMCA. Nevertheless, Mexico also has large bargaining power, as it has some leverage regarding migrant policies and could hurt the USA with retaliatory tariffs, especially on the agriculture. In any case, Mexico will face a challenging period, with a possible shallow recession ahead, depending on how far Trump pushes his agenda.

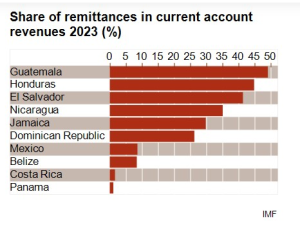

Harsher migration policies will affect Central American economies, liquidity and gang violence

Trump has pledged to close US borders and deport around 12 million undocumented immigrants. Although he may be restrained by the courts (as happened in his first presidential term), by American businesses and the logistical challenges of such an operation, he might reduce migrant populations in the coming years. Most immigrants living in the USA come from Central America and the Caribbean, and they play a significant role in the economies of their home countries by sending remittances back home. These remittances are crucial for household consumption, investment, poverty reduction and economic growth. Decreasing remittances would hurt the liquidity of those countries, as many Central American countries heavily depend on remittances for their current account revenues and foreign exchange reserves (see graph below). In this context, the short-term political risk rating of Central America has a negative outlook.

Moreover, a more closed America would have a ripple effect, as it would remove an essential economic pressure relief valve for Central America. Combined with fewer economic opportunities due to possibly reduced nearshoring (as Trump is focused on bringing industrial jobs back into the USA), lower economic growth and the likely end of development and aid programmes introduced by the Biden administration, this could make gang activities more attractive for people. As a result, gang violence and political violence is likely to increase in these countries. Moreover, in reaction to increasing violence, a harsh crackdown, as seen in El Salvador, could occur. While addressing gang violence often successfully, such measures could weaken democracy and institutions in the process. As a result, the political violence and expropriation risk ratings of Central America have a negative outlook as well.

Currency volatility and slower economic growth are likely in Latin America

Latin America will likely experience more currency volatility in the coming years due to Trump’s unpredictability and higher uncertainties in terms of policies. This could lead to tighter monetary policies in Latin America, resulting in higher borrowing costs for companies and slower economic growth in the region. In this context, the business environment risk rating of Latin America has a negative outlook. Additionally, under Trump’s presidency and amid expected higher geopolitical tensions between the USA and China, countries with strong Chinese ties (Cuba, Venezuela and Nicaragua), large trade relations (e.g. Brazil, Chile) or large Chinese investments in critical infrastructure like satellite communication or port infrastructure (e.g. Peru) will face stronger tensions with the USA and a higher risk of tariffs and sanctions. On the upside, a fiercer trade war between the USA and China could lead to trade diversion towards Latin America, and benefit those countries, as happened in 2018 when China redirected its soybean imports from the USA to Brazil.

Jolyn Debuysscher is a Latin America analyst with European credit insurance group Credendo.

Republished with permission.

RELATED ARTICLES

Trump and Latin America: Winners & Losers

Trump Tariffs Would Violate USMCA, FTAs

Fitch Warns of Trump Risk for Latin America

Latin America Most Exposed to Trump Risk

Moody’s Analytics: Trump Tariffs Would Cut Mexico Growth